Staking vs. Savings Accounts: Where Should You Park Your Money in 2025?

5 mins reading / Beginner

Staking and traditional savings accounts both offer ways to earn passive income, but they differ sharply in risk, returns, and accessibility. Discover why staking is the modern, high-growth alternative to a traditional savings account—tailored for the next generation of wealth builders.

What Is Staking? (A Simple, Clear Explanation)

Staking is a way to earn passive income with blockchain technology—taking the example of SOL tokens from the Solana network.

Here’s how it works:

1. You delegate your SOL tokens to a 'validator' like HIGH3R.

2. The 'validator' uses the delegation of your tokens to validate transactions over the Solana blockachin and secure the network.

3. In return, you earn staking rewards—currently around 8% APY—paid out automatically to your wallet every 2-3 days.

- You always keep ownership of your SOL tokens.

- You can unstake and withdraw them (after 2-3 days) whenever you want.

- Rewards are paid out automatically, and they are compounded automatically for even more growth.

When you stake your SOL tokens, you’re helping to keep the Solana blockchain running smoothly and securely.

Why Staking Beats Traditional Bank Savings Accounts

Let’s be real: traditional savings accounts just aren’t keeping up against price increase of goods (inflation).

Here’s why staking tokens is the better choice for ambitious savers:

- Much Higher Returns: Staking SOL tokens with HIGH3R now offers around 8% APY—well above the 3-4.5% offered by most savings accounts.

- Compound Growth: Your staking rewards can be automatically restaked, letting your SOL tokens grow faster over time.

- Direct Control: Your SOL tokens stay in your wallet. No banks, no middlemen—just you and the blockchain.

- Support Innovation: By staking, you’re actively supporting the future of finance and technology, not just funding a bank’s profits.

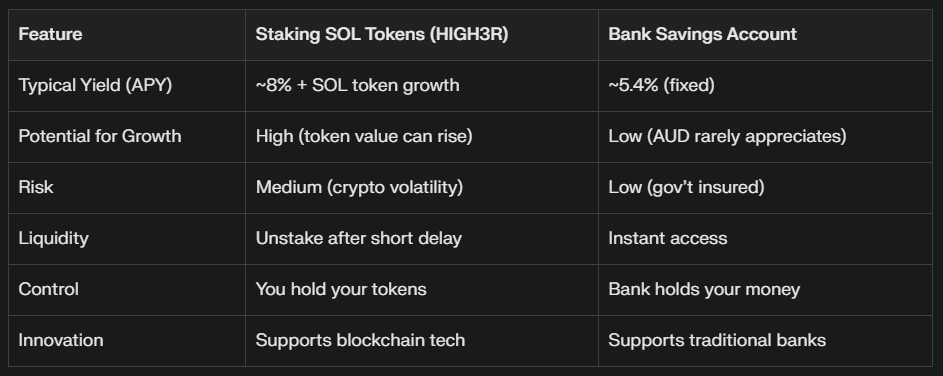

Staking vs Bank Savings Account: Quick Comparison

Real-World Example: How Much More Could You Earn?

Let’s say you stake $2,700 worth of SOL tokens for a year at 8% APY.

- Staking: You could earn about $216 in rewards, plus any gains if SOL tokens increase in value.

-Savings Account: You’d earn about $108, and your AUD stays flat.

If SOL tokens go up in price, your total could be much higher—something banks can’t match.

Frequently Asked Questions (FAQs)

Staking-Specific Questions

1. How do I choose a validator for staking SOL tokens?

Look for validators with high uptime (>99%), transparent fee and commision structures, and a track record of reliability.

2. What’s the minimum amount needed to stake SOL tokens?

Unlike some blockchains, Solana has no minimum stake requirement, making it accessible for beginners.

3. How are staking rewards calculated?

Rewards depend on the validator’s performance and the network’s inflation rate. On average, Solana stakers earn ~8% APY.

4. What happens if my validator misbehaves?

You'll stop receiving rewards, but you won't lose your tokens because they are in your wallet. Validators risk “slashing” (losing a portion of staked tokens) for malicious actions.

5. How long does unstaking take?

Solana has a 2–3 day cooldown period before unstaked SOL becomes available.

Savings Account FAQs

1. How is interest calculated on savings accounts?

Interest is typically compounded daily or monthly. For example, a 4% APY on $2,700 earns ~$108 annually.

2. Are bank savings accounts safe?

Yes—Australian deposits up to $250,000 are government-insured, making them virtually risk-free.

3. Can I lose money in a savings account?

No, but inflation (currently ~3%) erodes purchasing power over time.

4. Do I pay taxes on savings interest?

Yes—interest is taxable income. Staking rewards are also taxable but may offer deferral opportunities.

Comparative Questions

1. Which is better for long-term growth: staking or savings?

Staking offers higher growth potential through compounding and SOL appreciation, while savings accounts provide stability.

2. Can I access my funds quickly with staking?

Unstaking takes 2–3 days vs. instant access in savings accounts. Plan accordingly for short-term needs.

3. How do risks compare?

Savings accounts have near-zero risk (gov’t insured), while staking carries market volatility risk. Diversify based on your risk tolerance.

4. Are there hidden fees?

Some validators charge commissions (HIGH3R’s charges 0% commision), while banks may impose account fees if balances drop below thresholds.

Why Staking SOL Tokens Is the Smart Choice in 2025?

- Bigger returns, more control, and a chance to be part of the future.

- No hidden fees, no bank bureaucracy—just your SOL tokens working for you.

- Perfect for Australians who want to grow their savings and embrace new technology.

Related Searches

“How to stake SOL tokens in Australia”

“Best crypto savings options 2025”

“SOL token staking vs bank account”

“Is staking SOL tokens safe?”

Ready to start your staking journey?

Explore HIGH3R’s beginner-friendly platform, compare yields, and learn more in our educational hub.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Please do your own research and consult a financial advisor before investing.